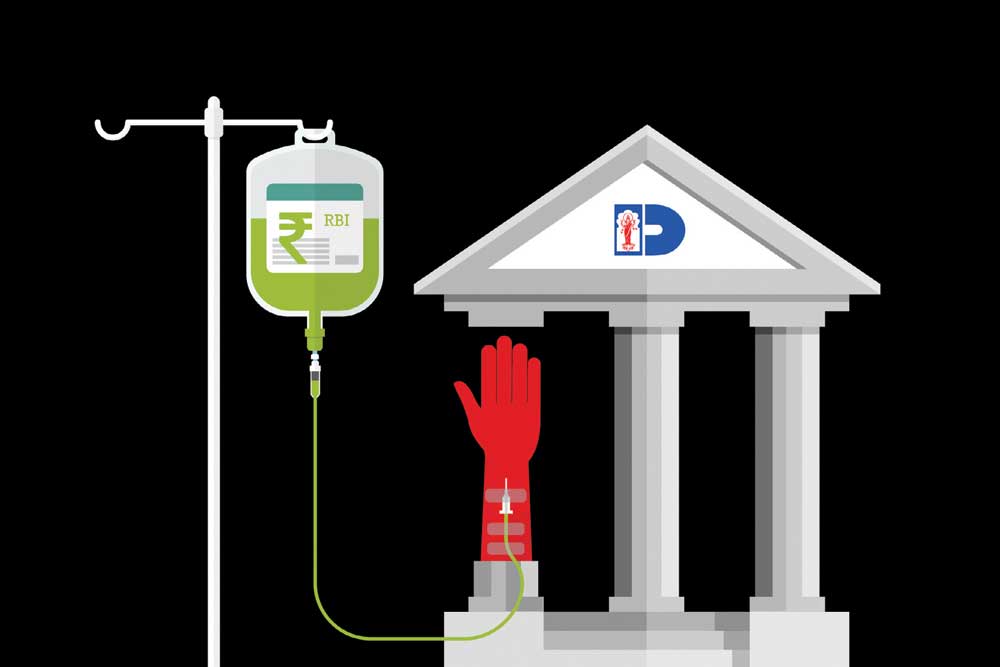

A BANKER I am acquainted with, who is the manager of one of the major branches of a PSU bank in a metropolitan city of India, says that his instructions from superiors are to not scout for new business. Instead, all energy is now to be focused on recovering bad loans. These loans go under the parlance of non performing assets (NPAs). For years, in what would be outright financial chicanery in any other sector, banks in India did not count alrge portion of such loans as NPAs until they grew so large that there was no hiding them anymore. For the last couple of years, all that banks have been scrambling to do is to clean up balance sheets, with little success. Some desperately needed Government assistance came in January, when the Finance Ministry announced that Rs 88,000 crore would be used to recapitalise banks. The crisis was thought to have been dealt with.

But it doesn’t seem to be going away anytime soon. In an extraordinary move, the RBI has just prevented Dena Bank from giving out new loans and also stopped it from doing any recruitment. The bank had been given Rs 3,000 crore in the recap scheme, but it has been of no consequence. A Hindu Businessline article had reported, ‘…nearly 70 per cent of the Rs 3,000 crore that the Centre infused into the bank, as part of its mega recap plan, has gone into absorbing bad loan provisioning in the March quarter alone. Dena Bank reported a net loss of Rs 1,225 crore in the March quarter, after providing for bad loan provisioning of Rs 2,150 crore. With the bank’s net NPA at about 12 per cent as of March 2018, it is close to breaching the third risk threshold under the RBI’s PCA framework.’

Consider if you were someone who had deposited his hard earned savings in Dena Bank. After receiving news like this, you would probably be running to take your money out. The only reason it does not happen is because there is an assurance that the Government will never let a PSU bank fail. While that is good for depositors, there must be someone who is paying to keep these banks alive, and is the taxpayer.

The RBI’s move is part of a strategy to get these ailing PSU banks to clean up their act and perform. As an Economic Times article said, ‘The government is looking to impose strict deadlines on banks that are under the Reserve Bank of India’s watch to implement a turnaround plan. This will include fixed targets for recoveries of bad loans, sale of non-core assets and a differentiated lending road map with each bank specialising in a particular area.’ This is however easier said than done. Decades of a non-competitive culture riddled with crony capitalism and Government interference can hardly be swept away by diktat or a carrot and stick policy.

That was not the only news this week to assail the banking sector. On May 14th, the CBI named a former Punjab National Bank head who is currently the chief executive of Allahabad bank in a chargesheet. This was in the case where jeweller Nirav Modi defrauded PNB of Rs 11,500 crore. The second largest PSU Bank in India is still grappling with the shock, but it didn’t have Modi alone to blame for its travails. A report in The Mint on May 15th noted, ‘The bank provided a colossal Rs 20,353 crore in the fourth quarter towards bad loans and fraud-hit accounts, but the Nirav Modi fraud accounted for less than two-fifths of this (Rs 7,579 crore)…The upshot: the bank has no growth capital left, even after qualified institutional investors put in Rs 5,000 crore and the government infused another Rs 5,400 crore this fiscal year. Fresh capital essentially went down a sinkhole of bad loans and fraud.’

The CBI chargesheet names other senior PNB officials too. When the scam broke, the bank had said that it was the doing of only a couple of renegade employees of a single branch. It now goes all the way up the ladder, as was always suspected. Also, the scam ran six to seven years and the question is how many more officials would have been complicit in it for it to have gone on for so long. The bad news is not over for either PNB or the country’s banking sector.

Private sector banks too have a problem with NPAs but market forces decide their fate and the taxpayer at least does not foot their bill. With PSUs, the support of the Government is a perpetual lifeline and politicians have long interfered in how loans were disbursed or who got promoted to the top post. The normal checks and balances of capitalism get skewed in PSU banks. The Government has little clarity on how to address the NPA mess. It has toyed with mergers to create big banks, but that plan seems to be on the backburner now. Fresh infusion of capital seems to have worked no magic. Punishing a bank by disallowing it from making loans or hiring seems impractical, given that it will have to soon blink and rescind the order. A long-term plan would be for the Government to get out of the business of banks altogether. It will probably not. Otherwise, how do you announce loans waivers for farmers before every election?

About The Author

More Columns

Travellers on Trial Bhavya Dore

Sahir’s Legacy Kaveree Bamzai

The Devi Mystique Bibek Debroy